Would you think I was crazy if I said retiring without a mortgage is a total bummer? After all, who in their right mind wouldn’t love to retire with no mortgage payment?

OK, so maybe I’m exaggerating a bit. Maybe it’s not a total bummer, but it’s a bummer nevertheless – and not for the reason you may think!

First of all, let me say it’s very commendable to pay off your house before retirement. Not having a mortgage payment makes it much easier to have a nice lifestyle on a fixed income. After all, your retirement income will be (or is) likely less than what you made in your working years.

An oft-cited reason retirees might choose to keep a mortgage is the mortgage interest deduction. Frankly, for most people, it makes zero sense to keep a mortgage simply for the tax deduction. The typical retiree saves far more by not having a mortgage payment than what they might save by writing off mortgage interest.

If you were thinking I was going to talk about mortgage interest deductions, let’s lay that to rest now. The real reason I think it’s a bummer to retire with no mortgage is something completely different.

Why retiring with no mortgage can be a bummer

To illustrate my point, let’s assume you worked your tail off and managed to retire with a free and clear home with no mortgage payment. Moving is a major pain in the backside, so you have no plans to sell your home in the future. This is your “forever home” where you plan to live the rest of your life.

According to US Census data, the typical American’s net worth at age 65 is $194,226. Of that, $150,304 is in the form of home equity. In other words, over 3/4 of the average 65-year old’s net worth is locked up in their home.

Now think about your home’s equity for a moment. What can you use it for? What practical impact does it have on your life? Sure, you have no mortgage payment, which is a good thing, but whether your home equity adds up to a dollar or a million dollars, how does it benefit your daily life?

The reality is that it’s just a number on paper, right? Sure, it might be a very nice number, but if you never plan to sell your home, that very nice number has little to no impact on your retirement lifestyle. After all, you can’t take your home equity down to a nice restaurant and exchange it for a steak dinner, right? You can’t use it to buy plane tickets to Hawaii . . . . right?

So, you busted your tail for decades, paid mortgage payments month in and month out, kept up with your property taxes, fixed things when they broke, and maybe even upgraded your home a bit. Maybe you got lucky and your home has even gone up in value. You’ve done everything right and managed to enter retirement with a nice net worth, but a large chunk of it is locked away in the form of unusable home equity!

Now that’s a bummer!!

How to solve the bummer

Having said that, there are ways to tap into home equity, but they either involve selling the home and cashing out all the equity (which means you have to find a new home) or doing a cash out refinance and saddling yourself with mortgage payments for the next 30 years.

Obviously, neither option makes a lot of sense if the goal is to enhance your retirement lifestyle without selling your house or taking on a payment.

If only there was a way to tap into your home equity without having to sell the house or take on a mortgage payment! How cool would that be?

Well, here’s the good news! You can turn home equity into a liquid retirement asset without selling or taking on a mortgage payment. Retiring with no mortgage doesn’t have to be a bummer after all!

How? With a home equity conversion mortgage, or HECM (often pronounced heck-um).

What the heck is a HECM?

The HECM is a federally-insured mortgage program designed to give you access to your home’s equity in retirement without giving up ownership of your home or taking on a mortgage payment. As long as you live in your home and pay the required property charges (property taxes and homeowner’s insurance), you can tap into a large portion of your home’s value without having to make mortgage payments.

No longer does home equity have to remain a largely “useless” asset that just looks pretty on paper. The HECM makes it possible to tap into that huge savings account called home equity and use it to enhance your retirement lifestyle.

If you owe little to nothing on your home, the ideal way to structure the HECM is as a line of credit. The line of credit is designed to convert a large chunk of your home’s value into what is essentially a tax-free retirement “account” that grows and compounds larger over time eith no limit.

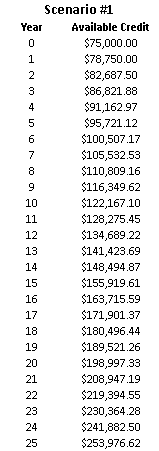

To see how the growth rate works, let’s take a look at an example. Let’s assume your home is worth in the $150,000 to $175,000 range and you qualify for an initial line of credit amount of $75,000. The annual growth rate is 5%, which is very reasonable for today’s market. Whatever remains unused in the line of credit is guaranteed to grow and compound based on the annual growth rate.

As you can see in Scenario #1, after just 5 years the line of credit will have grown to over $95,000. After just ten years, it will have grown to over $122,000. If you needed $122,000 for some reason, you could make a phone call and grab that cash, no questions asked, tax-free. Even better, you won’t be asked to make any payments on the money for as long as you pay your required property charges and live in the home.

As you can see in Scenario #1, after just 5 years the line of credit will have grown to over $95,000. After just ten years, it will have grown to over $122,000. If you needed $122,000 for some reason, you could make a phone call and grab that cash, no questions asked, tax-free. Even better, you won’t be asked to make any payments on the money for as long as you pay your required property charges and live in the home.

Because the growth rate applies to your available line of credit, growth compounds on growth. This means that the available credit in absolute dollar terms can really pile up over time.

The growth rate will also keep up with prevailing interest rates. If interest rates rise in the future, which is probably likely, the growth rate will increase as well, which means your line of credit will grow even faster.

Because there’s no limit on how much the line of credit can grow, it’s even possible it will grow larger than the value of your home! And because a HECM is non-recourse, you, your estate, and your heirs are not on the hook for any shortage if the home is worth less than the mortgage balance. The most that’s ever paid back is the value of the home, even if it’s worth less than the HECM balance.

What’s the catch?

So what’s the catch? There has to be one, right? Well, you have to be 62 years of age or older and own your home to be eligible. Ideally, your home is paid off (or nearly paid off) so you have a lot of equity to work with.

There are some income and credit qualifications, but as long as you have a reasonably decent income and pay your bills at least reasonably well, qualifying is usually not an issue.

There are some closing costs that have to be paid, but most (if not all) can be rolled into the new HECM balance.

The home equity “retirement account”

The HECM line of credit can be a powerful financial tool in retirement because it enables you to tap into that huge “savings” account called home equity without giving up ownership of the home or taking on a mortgage payment. Instead of home equity being a “sunk cost” and largely useless for funding your retirement lifestyle, you can now use it to live better in retirement and extend the life of your other retirement assets (IRAs, 401Ks, etc.).

Remember, the best part is that the line of credit will automatically grow and compound larger over time – with no limit! The program is designed to give you access to more money over time automatically, which provides tremendous financial security for the future.

So, not only have you now turned a “useless” asset – home equity – into a usable one that actually enhances your lifestyle, you’ve also turned it into an asset that performs for you. It grows and compounds larger with no limit – tax free!

Pretty cool, eh?

Maybe retiring without a mortgage doesn’t have to be such a bummer after all, right?