Credit card interest rates reached stratospheric new highs at the end of 2023. Consumers carrying credit card balances are now paying the highest average interest rates in at least the last thirty years.

Table of Contents

Credit Card Interest Rates Are At Three-Decade Highs

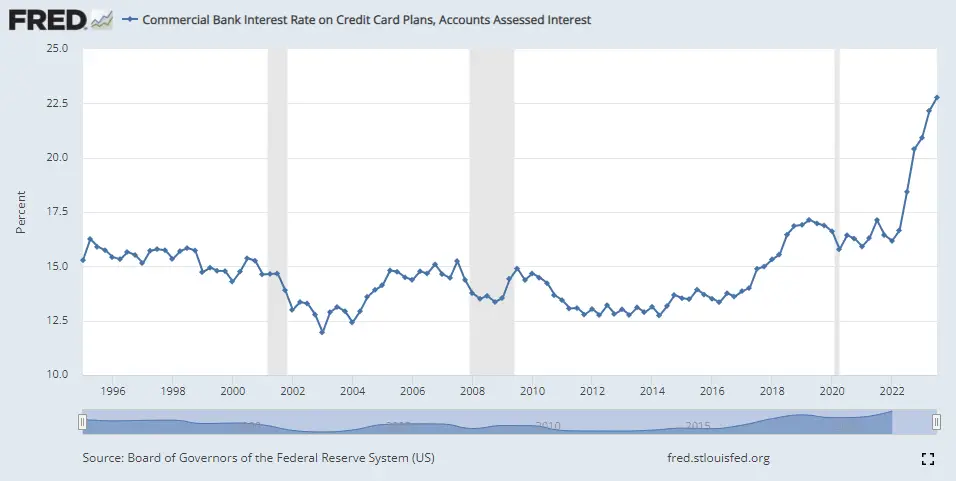

Consumers carrying large credit card balances are feeling the pinch of significantly higher credit card interest rates. At the end of 2023, credit card interest rates rose to the highest they’ve been in at least the last thirty years. Check out the chart below, which is from the Federal Reserve.

As you can see, the average credit card interest rate was around 15% from 1995 to the end of 2021. Since then, average rates have spiked to over 22.5%. That’s a stunning increase in a very short period of time.

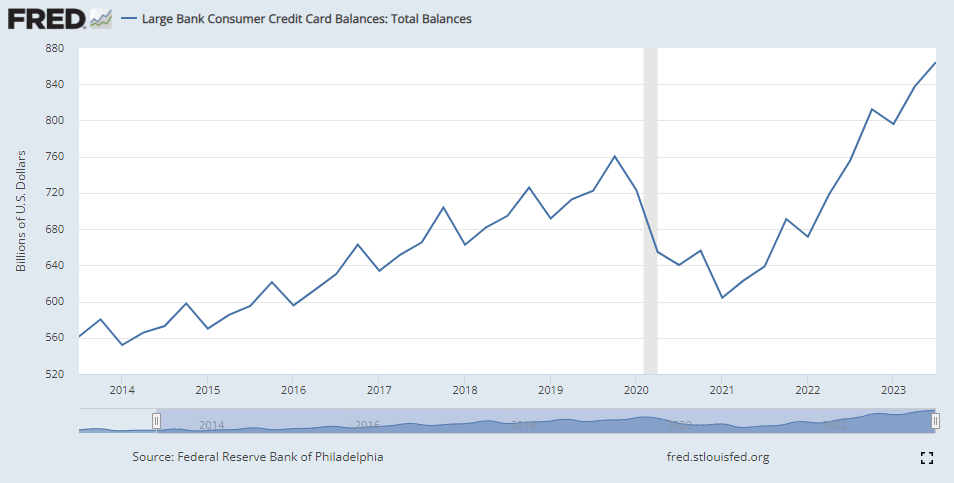

Unfortunately, the increase in credit card rates has come at the same time as an increase in credit card balances. Check out the chart below, which is also from the Federal Reserve.

As you can see, balances decreased substantially from late 2019 to the start of 2021. This coincides with record government stimulus during the COVID-19 pandemic. Many consumers used their federal stimulus checks to pay off credit card debt.

Mortgage rates were at record lows as well, so many consumers also paid off their credit cards with cash out refinances, HELOCs, or home equity loans.

Unfortunately, credit card balances didn’t stay down for long. They’ve since increased to new record highs since the start of 2021.

Thanks to the triple whammy of higher credit card rates, higher balances, and a sharply rising cost of living, it’s harder than ever for consumers to pay off credit card debt.

How Credit Card Minimum Payments Are Calculated

Credit card minimum payments vary depending on whether you have a large balance or a very small balance. Generally-speaking, here’s how credit card lenders calculate minimum payments:

- If you have a large balance – If you owe a large balance ($1,000 or more), then your minimum payment is likely around 2% of the balance. That’s enough to cover the interest and pay a small amount toward the principal.

- If you have a small balance – If your balance is relatively small (less than $1,000), then your minimum payment will probably be between $25 to $75, but never more than the actual balance itself.

Keep in mind that these are just general rules-of-thumb. Credit card lenders always want you to pay at least the interest, so if credit card interest rates increase, minimum payments will likely increase as well.

Minimum payments can be helpful if you have a month where expenses are tight. You can simply pay the minimum payment to stay in good standing. Obviously, you don’t want to make a habit of it because the finances charges are steep. If you pay just minimum payments, it could take ten to twenty years to repay your credit card balance – assuming you don’t increase the balance by charging even more.

Ways to Eliminate Credit Card Debt

Again, minimum payments largely get you nowhere when it comes to paying off your credit card debt. If you make just minimum payments, it could take ten or twenty years to pay off your debt. And with credit interest rates rising to record highs, it’s even tougher to pay off credit cards than just a few years ago.

Here are a few ways you can potentially eliminate your credit card debt:

- Make double or triple payments – If you have the free cash flow in your budget, you can wipe out your credit cards rapidly by doubling or tripling your minimum payments. If you have multiple credit cards, focus on the the smallest balances first. As you pay off balances, “snowball” the monthly savings into doubling or tripling your payments on the remaining credit card balances.

- Debt consolidation personal loan – A debt consolidation personal loan can be a great way to pay off credit card debt. The rates are typically fixed and often lower than credit card interest rates. The payments pay both principal and interest and the loan terms are usually 36 to 60 months.

- Debt consolidation HELOC – A home equity line of credit, or HELOC, can be a good way to consolidate debt into a lower monthly payment. However, keep in mind that HELOCs usually come with interest-only payments. You’ll need to make extra payments to actually pay the balance down. HELOC rates are usually much lower than credit card interest rates, which makes it easier to pay off your credit card debt faster.

- Home equity agreement (HEA) – A home equity agreement is a great way to tap into home equity without a monthly payment or interest charges, even if your credit is less than perfect. You can find more information about the home equity agreement here.

- Debt settlement – If you have a lot of debt and are struggling to pay it off, you may want to consider debt settlement. Debt settlement companies negotiate your balances down so you can get out of debt faster. Keep in mind that these types of programs will wreck your credit for a few years, so do this only if you are genuinely struggling to pay off your debt. You may also need to pay income taxes on the forgiven debt.

- Bankruptcy – This is a viable option, but should only be used as a last resort. Bankruptcy can eliminate your debt relatively quickly, but it’s a difficult process that will damage your credit for years to come.

When Will Credit Card Interest Rates Go Down?

So, what does 2024 hold for credit card interest rates? Will they drop this year? Honestly, it’s anybody’s guess. If inflation remains high, the Fed will keep interest rates high.

If the economy dips into recession and unemployment rises, the Fed may begin cutting interest rates, which could cause credit card interest rates to fall.

Rates will likely go down at some point, but there’s no way to predict when it will happen.

Frequently Asked Questions

Is 12% interest high on a credit card?

From 1995 to 2021, the average credit card rate was around 15%. From 2021 to 2023, average credit card rates spiked to over 22%. A 12% credit card rate is low compared to the average for the last thirty years.

What is 24% APR on a credit card?

APR stands for annual percentage rate. A 24% APR means you’re paying a 24% annual interest rate on balances not paid off by the end of the billing cycle.

What does a 20% interest rate on a credit card mean?

A 20% interest rate on a credit card means you’re paying 20% annual interest on balances not paid off by the end of the billing cycle. For example, if you carry a balance for one year on a credit card with a 20% interest rate, you’ll end up paying about $200 in interest (20% of the balance).

What is a good interest charge on a credit card?

From 1995 to 2021, the average credit card rate was around 15%. From 2021 to 2023, average credit card rates spiked to over 22%. Anything below 22% is probably good these days. Having said that, ideally, you don’t want to carry a balance at all. Instead, try to pay off your credit cards in full at the end of each billing cycle. The best interest charge is no interest charge at all.