Rising interest rates have pummeled the reverse mortgage industry in 2023. According to the latest HUD HECM Snapshot, reverse mortgage endorsements are down significantly over the last year. Fortunately, it’s not all bad news. There are some intriguing bright spots in the data.

It’s a good bet you’ve been hearing a lot about rising rates lately. The Federal Reserve has been aggressively increasing interest rates to try and get inflation under control. I’ve been through a number of rate cycles as a mortgage professional, but even I’m surprised at how far and fast interest rates have risen over the last year.

Rising interest rates have pummeled the reverse mortgage industry, according to the March 2023 HUD HECM Snapshot. Rates are up and endorsements are down significantly, but there is some positive news as well.

I’ve summarized the most important and interesting data points in the infographic below. If you’d like to embed the infographic on your website, simply copy the code in the box below and paste it into the page where you want the infographic to appear.

If you’d like additional insights into the data points we’ve presented, you can find them further down the page.

Table of Contents

INFOGRAPHIC: Rising Rates Pummel The Reverse Mortgage Industry

If you’d like to embed this infographic on your website, simply copy the code below and paste it into the web page where you want it to appear.

Interest Rates Take Their Toll on the Mortgage Industry

I’ve logged a lot of years in the mortgage industry and I’ve never seen interest rates increase so far so fast. In early 2022, 30-year fixed interest rates averaged in the 3% to 4% range. By the end of the summer, they were in the 6% to 7% range for most borrowers.

Unsurprisingly, rapidly rising interest rates have triggered a bloodbath in the traditional “forward” mortgage industry. Funding volume plummeted and many lenders closed up shop, discontinued loan products, and laid off staff.

Refinance transactions are the lifeblood of “forward” mortgage lenders, but they’ve all but dried up because nobody with a pandemic-era 3% rate wants to refinance into a 7% rate. Home purchase volume has also crashed because rising interest rates have made homes unaffordable for many buyers.

As of this writing, mortgage applications are nearly the lowest they’ve been in 30 years.

The reverse mortgage industry has also taken a hit, but the damage is less severe. Yes, interest rates are up and endorsements are way down, but reverse mortgages tend to be less rate sensitive than “forward” mortgages. Many homeowners can still find value and benefit in a reverse mortgage even though rates are higher.

What Does “Endorsement” By FHA Mean?

“Endorsement” by FHA represents the final completion of a HECM reverse mortgage. When FHA endorses a reverse mortgage, it insures the reverse mortgage, which makes it a non-recourse loan. Only reverse mortgages that meet FHA’s HECM guidelines will receive endorsement.

How Rising Rates Impact Reverse Mortgages

The most common reverse mortgage in the United States is the FHA-insured home equity conversion mortgage, or HECM (often pronounced heck-um by industry insiders).

If you’re at least 62, a HECM enables you to borrow against your home equity on a non-recourse basis without a mortgage payment and without giving up ownership of your home.

Traditional “forward” mortgages are more rate sensitive because monthly payments tend to increase with rising interest rates. A reverse mortgage has no mortgage payment as long as at least one borrower (or non-borrowing spouse) lives in and maintains the home and pays the required property charges.

That said, rates do impact reverse mortgages to some extent. The effects of rising interest rates show up in a few different ways – some obvious and some not so obvious:

- Higher interest costs – This is obvious, right? A reverse mortgage is a home loan, so higher interest rates lead to higher interest costs on new and existing HECMs. Most HECMs have variable interest rates because the variable-rate HECM is more flexible and usually offers the most money. The downside to the variable-rate HECM, however, is that interest accruals increase as interest rates rise.

- Reduced proceeds – HECM proceeds are calculated in part based on current interest rates. As interest rates increase, proceeds tend to decrease. Average HECM proceeds have decreased over the last year as rates have risen, which has made qualifying difficult for many homeowners with large mortgage balances.

- Lower home values – Home values are sensitive to interest rates because most home buyers use a mortgage to purchase a home. Higher mortgage rates result in higher mortgage payments. If mortgage rates increase enough, home values must fall to keep homes affordable for the average buyer. HECM proceeds are calculated as a percentage of home value, so a reduction in home values results in a reduction in HECM proceeds.

- Higher line of credit growth – As crazy as it sounds, higher rates are actually beneficial for many reverse mortgage borrowers. Line of credit growth is one of the most attractive features of a HECM reverse mortgage. Line of credit growth rates tend to follow prevailing interest rates, which means growth rates have increased significantly over the last year. Homeowners who have a HECM line of credit are enjoying some of the best line of credit growth rates they’ve likely ever seen.

How Rising Rates Have Impacted The Reverse Mortgage Industry

According to the latest HUD HECM Snapshot, it’s been a rough year for the reverse mortgage industry. Yes, reverse mortgage production is down significantly in 2023, but it’s not all bad news. There some interesting bright spots in the data. Let’s cover the bad news first:

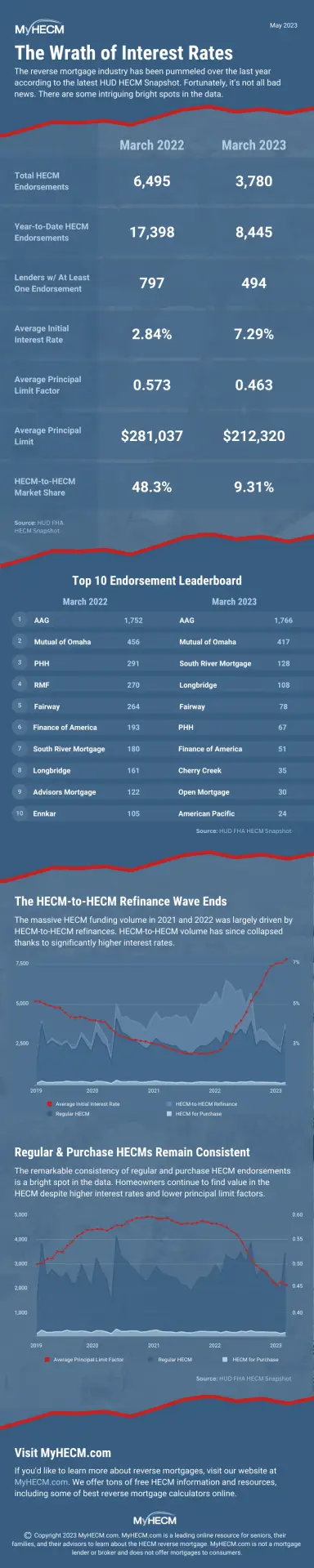

- Total HECM Endorsements – HECM endorsements declined from 6,495 in March 2022 to just 3,780 in March 2023. That’s a massive 42% decrease in just a year!

- Year-to-Date HECM Endorsements – HECM endorsements fell from 17,398 in the first quarter of 2022 to just 8,445 in the first quarter of 2023. That’s a 51% decrease!

- Lenders With At Least One Endorsement – The number of lenders with at least one endorsement declined from 797 in March 2022 to just 494 in March 2023. Significantly fewer companies are writing reverse mortgages this year versus last year.

- Average Initial Interest Rate – The average HECM initial interest rate increased by a stunning 250% from 2.84% in March 2022 to 7.29% in March 2023.

- Average Principal Limit Factor – A principal limit factor (PLF) is used to calculate proceeds. PLFs and interest rates have an inverse relationship, which means PLFs decrease as interest rates increase. This is why the HECM tends to offer less proceeds as interest rates rise. The average principal limit factor decreased from 0.573 in March 2022 to 0.463 in March 2023. Home values continued to increase in many markets until the summer of 2022, so the PLF decrease was offset somewhat by higher home values. However, current HECM applicants are qualifying for a significantly smaller portion of their home’s value than they did a year ago.

- HECM-to-HECM Market Share – Many homeowners refinanced their reverse mortgages during the pandemic to reduce their interest rates and/or qualify for more proceeds. In March 2022, half of all HECM endorsements were HECM-to-HECM refinances. As interest rates started to rise, HECM-to-HECMs no longer made sense and began to dry up. The HECM-to-HECM market share has since collapsed from 48.3% in March 2022 to just 9.31% of the market in March 2023.

The Top 10 Leaderboard Shakeup

The top 10 leaderboard has seen some interesting changes over the last year. As you can see, most HECMs are funded by a relatively small number of lenders.

AAG has been the dominant player in the industry for a number of years now, but other lenders like Longbridge Financial and Mutual of Omaha have been gaining market share.

The most notable change on the top 10 leaderboard is the disappearance of Reverse Mortgage Funding (RMF). Unfortunately, they went bankrupt last fall.

AAG appears to have gained over the last year, but their March 2023 endorsements are an outlier. In March 2023, AAG was in the process of being acquired by Finance of America (also on the leaderboard). AAG was likely rushing to fund out their loan pipeline before the completion of the acquisition.

As you can see, most lenders have seen a significant decline in endorsements over the last year. Other than AAG, Mutual of Omaha is the only lender on the list who has largely maintained their funding volume.

The HECM-to-HECM Refinance Wave Ends

This graph is interesting because it shows the changes in the transaction type mix since 2019. As you can see, HECM-to-HECM refinance volume exploded when rates fell during the pandemic. Now that rates have increased, HECM-to-HECM endorsements have utterly collapsed.

Lenders who focused on the low hanging fruit of HECM-to-HECM refinances over the last few years have likely seen their endorsement volume plummet.

Some Bright Spots in the Endorsement Data

The reverse mortgage industry has been a depressing place for many lenders and originators since late 2022. To some extent, this is understandable. After all, higher rates results in lower principal limit factors, reduced proceeds, and fewer reverse mortgages that work.

However, I want to point out a bright spot in the last chart on the infographic, which shows endorsements and average principal limit factors since 2019.

As you can see, principal limit factors have changed significantly over the last four to five years. They increased as interest rates fell, then they decreased as interest rates rose.

In other words, homeowners received a larger portion of their home’s value as interest rates fell during the pandemic. When the pandemic ended and the Fed began increasing rates, homeowners started to receive a smaller portion of their home’s value.

As you can see in the chart, regular and purchase HECMs have remained remarkably consistent over the last four to five years – even as HECM rates more than doubled. Homeowners clearly still find value in the HECM even though interest rates are higher and principal limit factors are lower.

This is good news for lenders who focus on finding value for their clients. If you’re an originator who focuses on rates and dollar amounts, your business is probably suffering. If you’re focused on how a reverse mortgage provides benefit despite higher interest rates and lower principal limit factors, you’re probably still seeing success.

Are Reverse Mortgages Still a Good Deal?

Now that rates are higher, is the reverse mortgage still a good deal? Absolutely! Homeowners continue to take advantage of a HECM to eliminate mortgage or other debt payments, fund home improvements, pay off medical bills, and supplement retirement income and assets.

Homeowners who owe little to nothing on their homes are jumping all over the HECM line of credit because the growth rates are phenomenal right now. If you’re at least 62 and your home is free and clear, you may want to check into the HECM line of credit even if you don’t need the money right now. Just set up the line of credit and let it grow. By the time you need it, it will have a much larger dollar amount in it than when you set it up. Every dollar added to your credit line equals increased financial security for your retirement years.

I freely acknowledge that a reverse mortgage isn’t always the perfect solution for every senior. However, it’s still a great option for many homeowners even in today’s interest rate environment.

What happens when interest rates rise?

Rising interest rates cause the economy to slow down and potentially enter a recession. Rising interest rates discourage borrowing, which means less money is invested into the economy to stimulate spending, investment, job creation, and economic growth.

Who benefits from high interest rates?

Savers benefit from higher interest rates because their bank deposits earn more interest. Rising interest rates encourage people to save, which helps refill the nation’s capital base and set up the next economic expansion.

How do interest rates affect inflation?

When rates are low, it stimulates economic activity. If too much economic activity is stimulated, it can cause price inflation. The Federal Reserve increases interest rates to slow down economic activity and reduce inflation.

How many rate hikes in 2023?

Only the Federal Reserve knows the definitive answer to this question. However, with the latest rate hike in May 2023, the Fed has signaled a potential “pause”. How long that pause will be depends on what happens with inflation and the economy.