Updated 8/2/2023 – If you’re not familiar with the term sequence risk, you definitely should be. It’s a potentially devastating lurking danger that can completely swamp an otherwise solid retirement plan. Brian Davis wrote a great article over at Bigger Pockets on this topic a while back and I’d like to build on what he wrote. If you haven’t read his article yet, you may want to now. I’ll hang tight until you get back :).

As Brian defined it, sequence risk is “the risk that the market (usually the stock market, but technically any market you’re invested in) will crash within the first few years of your retirement”. Sequence risk is dangerous for your financial well-being in retirement because it can cause you to burn through your savings faster than expected.

To illustrate this risk, let’s assume you recently retired and need $1,000/month in income from your Roth IRA. Let’s also assume you’re 100% invested in a balanced ETF that is trading at $50/share. To meet your income needs, you need to sell 20 shares every month to achieve your $1,000/month income target (20 shares * $50 = $1,000).

But what if the price of your balanced ETF crashes by 50%? You now need to sell 40 shares to meet your income needs. You’re now draining your shares twice as fast, which means you risk running out of money earlier than planned.

The old adage “buy low, sell high” is applicable; you want to be a seller when the market is up, not down. If the market is down, you want to have other financial options to meet your income needs so you don’t have to sell low.

Defending against sequence risk

The whims of the financial markets are beyond our control, so the best defense against sequence risk is to have multiple financial options. You want to have multiple income sources so you aren’t forced to draw draw down an asset when market conditions are unfavorable. Brian highlighted a few possibilities, including real estate and cash savings, but I’d like to offer another option you’ve probably never thought of: home equity.

The equity in your home can be an important defense against sequence risk. If the stock market is bad, you can rely on home equity to fund your lifestyle instead of selling shares into a bad market. When the stock market recovers, you can leave your home equity alone and once again live off your investments. This enables you to preserve both your lifestyle and your retirement savings for longer.

Two ways to tap home equity (one good, one not so good)

Let’s address two ways – one good, one not as good – that retirees commonly tap home equity to fund their retirement. Let’s cover the bad one first.

Many seniors rely on a HELOC, or home equity line of credit, for their cash needs in retirement. I’ll be honest with you: I cringe when I meet seniors who have HELOCs because I know the financial headaches they can cause.

Now don’t get me wrong, I have nothing against HELOCS. A HELOC is a great product, but only when it’s used for the right purpose. Unfortunately, many seniors use them for the wrong purpose (often at the recommendation of well-meaning advisors) and end up getting into trouble.

HELOCs are designed for short-term cash needs where you borrow and repay on a relatively short-term basis. Unfortunately, many seniors use HELOCs as a long-term cash source and carry large (and often growing) balances for many years. This can be highly risky for several reasons:

- Interest-only payments. Most HELOCs have low minimum payments that only cover the interest. Unless you intentionally make extra payments, the debt isn’t paid down over time.

- The more you borrow, the bigger the payment. This can become a real financial headache if you use a HELOC to cover big expenses such as medical bills, car repairs, or home maintenance. The more you borrow, the bigger the payment gets.

- Adjustable rates. Though some HELOCs have fixed rates, most come with adjustable interest rates. If rates rise, the payment will as well, which further exacerbates problem #2 above.

- HELOCs can be revoked, chopped, or frozen with little notice. This can be bad news if you plan to use the HELOC as a long-term financial safety net. If home values fall or credit conditions deteriorate, banks will reduce their risk exposure. It’s entirely possible your HELOC will be revoked, chopped, or frozen when you need it most.

- HELOCs are typically full recourse loans. If home values fall and you owe more than the home is worth, the bank may come after you for the shortage if you try to sell your home. You will either have to come up with a lot of cash at closing or negotiate a short sale to get your home sold. And if you can’t keep up with the payments, you may face foreclosure and a deficiency judgment for the unpaid loan balance.

- The recast. This is probably one of the most devastating problems with HELOCs. Unfortunately, most homeowners only discover this financial iceberg when they’re about to crash full-on into it. Most HELOCs allow you to withdraw funds for up to the first ten years of the loan term. At the ten-year mark, the bank recasts the loan into a full principal and interest payment that pays back the entire balance over a relatively short time period. If your balance is large, this can mean your payment increases by hundreds of dollars or more. I can think of one particular client a few years ago who had this happen to her. She’d had her HELOC for 10 years and the payment recast from a manageable $150 to over $700. Because she was on a fixed income, she struggled to make the payment and was at risk of losing her home. Ten years might seem far off, but the years pass quickly. You don’t want to be in your late 70s or 80s, potentially in declining health, and facing the loss of your home.

In short, the HELOC is not designed to be a source of income (or emergency funds) in retirement. They’re just too risky, in my opinion.

So, what’s a far better solution? The HECM line of credit. This is the good way to tap into home equity in retirement.

The convenience of a HELOC, but without the risk

A HECM, or home equity conversion mortgage, is a federally-insured home loan that enables homeowners 62 or older to convert a large portion of their home’s value into tax-free cash without giving up ownership of the home or taking on a mortgage payment. As long as at least one borrower is living in the home and paying the required property charges (property taxes, homeowners insurance, etc.), no mortgage payments are required.

HECM proceeds can be received as a lump sum, monthly term or tenure payment, or line of credit.

It’s the line of credit that I want to focus on here because it can help defend your savings against sequence risk.

The beauty of the HECM line of credit is that it has the flexibility and convenience of a HELOC, but without the payment risk. Again, as long as a least one borrower is living in the home and paying the required property charges, no payments are required.

The best part is that the unused credit line grows and gives you access to more of your equity over time automatically based on a guaranteed growth rate. A HELOC definitely doesn’t do that!

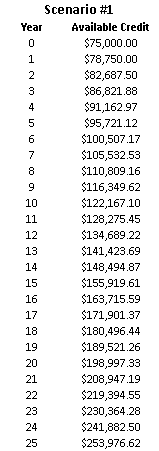

To see how the growth works, let’s take a look at an example.

Let’s assume the initial credit line is $75,000 and the annual growth rate is 5%. As you can see in the table, after just 5 years, the line of credit will have grown to over $95,000. After ten years, it will have grown to more than $122,000!

Let’s assume the initial credit line is $75,000 and the annual growth rate is 5%. As you can see in the table, after just 5 years, the line of credit will have grown to over $95,000. After ten years, it will have grown to more than $122,000!

Because the growth rate applies to the available line of credit, growth compounds on growth. This means that the available credit in absolute dollar terms can really pile up over time – especially if you get it set up early in retirement.

Even better, the growth rate is designed to keep up with prevailing interest rates. If rates rise in the future, the growth rate will rise as well, which means the line of credit will grow even faster.

Because there’s no limit on the size of the line of credit, it could even outgrow the value of the home at some point. If that happens, you’ve beat the system! Remember, the HECM is a non-recourse loan, which means the most that has to be paid back is the value of the home. FHA will cover any shortage out of it’s insurance fund.

The HECM line of credit essentially turns a large chunk of your home’s equity into a liquid and tax-free retirement “account” that grows.

More options equals more financial security

I think it is absolutely essential to have as many financial options in retirement as possible. People are living longer, the cost of living is rising, and there’s a lot of economic uncertainty out there.

When you’re retired, you simply don’t have the capacity to earn an income the way you did in your younger years. It’s essential to protect and preserve your assets against the risks of the economy and financial markets. Just as it’s prudent to diversify your investments, it’s also prudent to diversify your income sources to protect your lifestyle and savings from sequence risk.

The HECM line of credit can be a fantastic addition to an already solid financial plan for retirement. When the financial markets are down, you can live on home equity. Once the markets recover, you can leave your home equity alone and once again tap into retirement accounts for your income. The end result is that you protect and preserve your assets and lifestyle for longer.