Nobody wants to run out of money and be financially shipwrecked in retirement. Unfortunately, there is a lurking and potentially devastating danger out there that can wreck even the best of retirement plans. In this article, I’d like to lay out a unique and little-known strategy (even to financial planners) that can help protect your retirement savings and preserve them for longer.

One of the most devastating financial risks in retirement is one many people have never even heard of. Unfortunately, many retirees fall prey to this danger completely unaware of it and end up running out of money years sooner than expected. What is this danger? It’s sequence risk, or sequence of returns risk. My goal with this article is to detail a unique and little-known strategy that can significantly reduce sequence risk, which can help protect your retirement assets, lifestyle, and financial security for much longer.

Will your money last at least as long as you?

Most people save for retirement during their working years by buying stocks, mutual funds, ETFs, etc., through a 401(k) or IRA. They build up a retirement nest egg by accumulating shares that (hopefully) increase in value and/or generate a return over time.

When you retire, you do the opposite. You’re no longer working, so you sell shares in your retirement account and use the proceeds as income. The challenge is striking the right balance between generating income and preserving your assets so they last at least as long as you do. If you drain your assets too fast, you risk running out of money before you die. If you don’t withdraw enough, you’ll protect your savings for longer, but risk missing out on the retirement lifestyle you worked decades to earn.

Many financial professionals and pundits like to point out that the S&P 500 stock index has achieved a 10% average return since its inception in 1928. That’s a great statistic, but it’s a bit misleading. After all, the stock market doesn’t go up in a steady and straight line. If it did, saving for retirement would be pretty easy, right? The stock market goes up and down and over the long term it returns the average 10% we all hear about.

What kind of market will it be when you retire? Will you get lucky and retire at the start of a long bull market? What if you retire at the start of a devastating bear market? What if the value of the shares in your retirement account drops by half just as you quit your job? If your shares drop by half, you now need to sell twice the number of shares to achieve the same income target. You’re now draining your retirement assets faster, which means you’re at risk of running out of money sooner.

This is the essence of sequence risk. It’s the risk you’ll encounter a bear market early in retirement, causing you to drain your retirement assets faster than expected. Sequence risk is that lurking predator waiting to devour the assets you worked hard to build during your working years. It’s almost impossible to see it coming because it’s impossible to predict exactly when the next bear market will begin.

When you’re retired, you don’t have the capacity to earn like you did in decades past. If you want a financially secure retirement and want to defend against sequence risk, it’s essential to have as many financial options as possible. To show how a reverse mortgage can help reduce sequence risk and protect your retirement savings for longer, let’s look at a few scenarios based on real-world data. Note that we’ll disregard income taxes for the sake of simplicity.

Scenario #1: How sequence risk destroys retirement assets

Let’s assume it’s January 2007 and Andrew, a former accountant, has just retired with a free and clear house and a 401(k) worth $191,900. To protect his nest egg, Andrew plans to move his entire 401(k) into ABALX, a conservative balanced mutual fund (note this isn’t investment advice; it’s just for example purposes). Balanced funds are often preferred by retirees because they’re diversified over a variety of assets to provide safer and more conservative returns.

Andrew recently started taking Social Security, but it isn’t enough to cover his expenses. He plans to withdraw $1,000 from his 401(k) every month to make up for the income shortfall.

Andrew moves his 401(k) into ABALX at the end of September 2007 and purchases exactly 10,000 shares at $19.19/share. He takes his first $1,000 withdrawal at the beginning of October 2007.

Well, we all know what happens next, right? The stock market declines badly all through 2008 and finally bottoms in early 2009. Unfortunately, as the share price of ABALX falls, Andrew is forced to sell more shares to achieve the same $1,000 income he needs to cover his expenses.

Back in October 2007, he only needed 53 shares to yield $1,000 ($1,017.07 to be exact). At the market bottom in February 2009, it takes 84 shares to get $1,000. Yikes! He’s draining his assets much faster than planned and he’s starting to worry. He’s just two years into retirement and he’s already sold over 1,500 of his original 10,000 shares of ABALX.

Andrew is confident the market will recover, but when? He’s burning through shares so fast he’ll have hardly any left to rebuild his account balance once the market recovers. The market will recover at some point, but will his account last until then? Andrew needs the income, so he hopes for the best and continues taking his $1,000 every month.

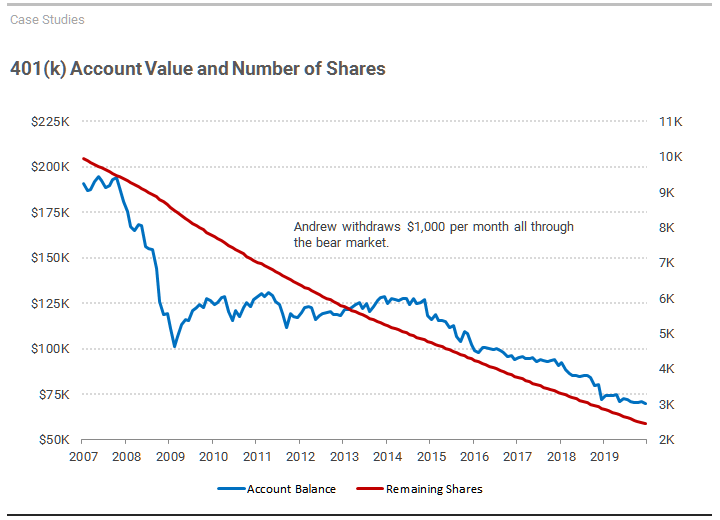

Now, let’s fast forward to December 2019. How is Andrew’s 401(k) holding up? Unfortunately, not well. Figure 1 shows the damage done to his account balance. The 10-year bull market since 2009 has increased the value of his remaining shares, but his account balance is now just under $75,000. Andrew has only 2,447 of his original 10,000 shares left. He’s blown through over 3/4 of his shares in twelve years. Not good! Andrew is in danger of running out of money much earlier than anticipated.

Unfortunately, Andrew’s 401(k) and future financial security have fallen prey to sequence risk. He needed the income to cover his expenses, so he had no choice but to be a seller during the bear market years. He’s drained his 401(k) and is facing the very real prospect of outliving his money.

Now, what if Andrew had another asset to rely on in addition to his 401(k)? What if he was able to add home equity to the retirement picture? What if he could have tapped into that equity (without taking on a mortgage payment) so he didn’t need to sell his retirement account shares into a declining market? As we’ll see, he not only would have had more money to live on, but he would have helped protect his retirement savings for much longer.

Scenario #2: How to protect your retirement savings for longer

Let’s take a time machine back to January 2007 and once again assume Andrew has just retired with a free and clear home. This time, however, let’s assume his financial advisor has told him how he can tap into home equity without a mortgage payment using a home equity conversion mortgage, or HECM. Andrew does a little research on the HECM and discovers that he can take the proceeds using a line of credit that will grow and compound larger over time. Andrew is intrigued! He figures he has tons of home equity just sitting there doing nothing, so he wants to use it to make himself more financially secure. It’s a good idea to have as many financial options as possible, right? After all, you never know when the next bear market might hit, right?

By the way, if you’re not familiar with how a HECM works, you may want to cover some basics before reading further. There are a lot of myths and misconceptions floating around about the HECM.

Let’s assume that, according to a HECM calculator, Andrew starts off with a line of credit of $100,600 with an annual growth rate of 5.96%. Andrew’s plan is to leave the line of credit untouched and let it grow until he needs it.

Let’s again assume Andrew moves his 401(k) into 10,000 shares of ABALX in September 2007. As before, he sets up a $1,000/month withdrawal that will start in October 2007. Just a few days before receiving his first check in October 2007, Andrew gets nervous about the markets. He’s seen the headlines about subprime mortgages how they may impact his the financial markets. He decides to cancel the withdrawal from the 401(k) and begin taking $1,000/month from his HECM line of credit instead. By this time, he’s already enjoyed 10 months of growth and his line of credit is now worth $105,187.

Well, we all know what happened in the stock market in 2008 and 2009. It’s painful to watch his 401(k) decline in value, but Andrew holds firm with the belief that it will recover at some point. In the meantime, at least his income is secure and he’s not selling shares into a declining market.

Andrew leaves his 401(k) completely untouched while the market declines. In fact, he leaves the 401(k) untouched for a full five years until it once again recovers back to the same value it was in September 2007.

In September 2012, Andrew decides to stop his withdrawals from the line of credit and instead start taking money from the 401(k). His first $1,000 payment from the 401(k) arrives in October 2012. His 401(k) is now worth $200,393 and the available HECM line of credit is worth $71,911. Andrew has a total of $272,304 in liquid assets available. Not bad, right?

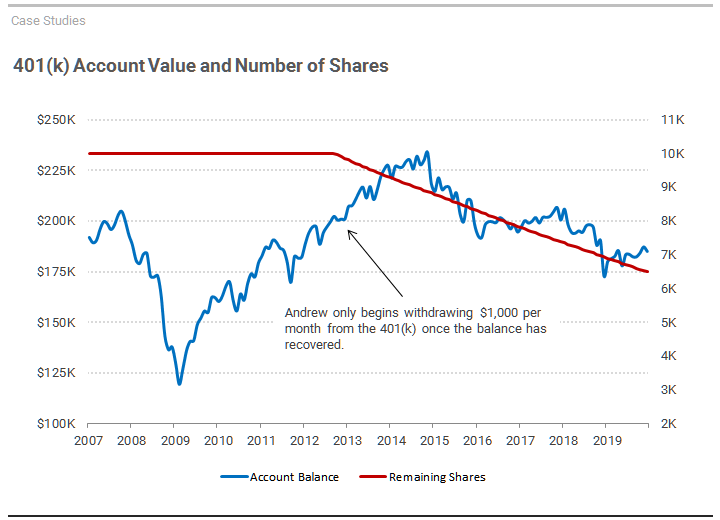

Let’s fast forward to December 2019 and see how things look. Andrew has left his HECM line of credit alone for the last seven years to let it grow and has continued to draw $1,000 per month from his 401(k). Check out the results in Figure 2.

As of December 2019, the 401(k) balance is $184,993. That’s just a little less than where it started over a decade ago! Yes, the balance took a hit through the bear market of 2008 to 2009. However, Andrew recouped the losses because he had another income source and wasn’t forced to sell during the downturn. He preserved more than $100,000 worth of account value versus Andrew in Scenario #1. Even better, the HECM line of credit still has $110,112 available. That too, is roughly the same amount as when he retired nearly 12 years ago.

By having more than one financial option, Andrew was able to choose what asset to tap based on market conditions. He was able to protect retirement savings and insulate his lifestyle from a nasty bear market.

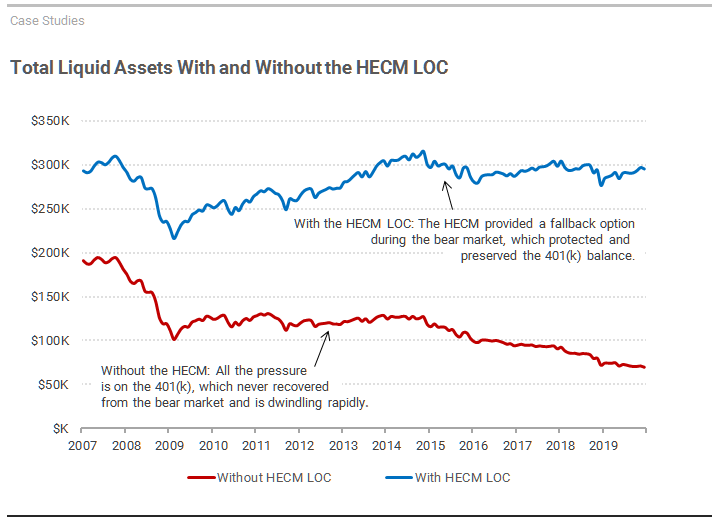

As you can see in the Figure 3, below, the results speak for themselves. The Andrew in Scenario #1 (the bottom line in red) has already burned through well over half of his liquid retirement assets by the end of 2019. This is especially worrisome because another bear market will likely wipe him out completely.

On the other hand, the Andrew in Scenario #2 (the top line in blue) has done far better. Because he had multiple financial options, he could choose what asset to live on based on market conditions. He not only protected his savings, he ended up with $200,000 more to live on than Andrew in Scenario #1.

We have a winner!

Folks, it’s pretty clear: 401(k) plus HECM line of credit is the winner against the sequence risk monster. The HECM line of credit can help protect your retirement savings and lifestyle for much longer. There is tremendous financial security in having multiple financial options. If you have more than one income source, you can more effectively protect your assets and lifestyle against market downturns. You can pick and choose what income source to tap into based on market conditions. If a downturn hits your retirement account, leave it alone and use the HECM until the market recovers. Once the market recovers, you can live on your retirement savings and leave the HECM line of credit alone.

If you liked this article, please click “Follow” on our LinkedIn page.

This article is an excerpt from The Reverse Mortgage Revealed: An Insider’s Guide to the Reverse Mortgage, which has been recently updated and expanded and is available now on Amazon. Get your copy today!

If you’d like to see how much you may be able to get from a HECM reverse mortgage, feel free to check out our HECM calculator.

Image by Steve Buissinne from Pixabay.