If there’s one constant in the reverse mortgage industry, it’s change. FHA has once again made some significant tweaks to the HECM program to make it work better and be more stable for seniors.

This latest round of changes is a bit of a mixed bag; there’s both positives and negatives for reverse mortgage borrowers, depending on how you look at things.

IMIP Is Now a Flat Rate

Before the changes implemented this week, the IMIP rate would be based on how much is borrowed at closing. If less than 60% of the principal limit was utilized at closing, then the IMIP rate was 0.50% of the maximum claim amount (the appraised value for most borrowers).

If more than 60% of the principal limit was borrowed at closing, then the IMIP increased to 2.50% of the maximum claim amount.

FHA is now assessing a flat 2% of the maximum claim amount for all borrowers, regardless of how much they borrow at closing.

For borrowers with a high utilization (such as when a big mortgage is being paid off), this is great news because it’s a 0.50% reduction. On the other hand, borrowers who owe little to nothing on their homes are now being charged 4 times more than they would have been before the changes.

Annual MIP Has Been Reduced

Before the changes, the annual MIP was assessed at an annual rate of 1.25% of the mortgage balance. This has now been reduced to 0.50%, which is great news for all reverse mortgage borrowers. This means that the loan balance will grow more slowly over time and your equity will be preserved for longer.

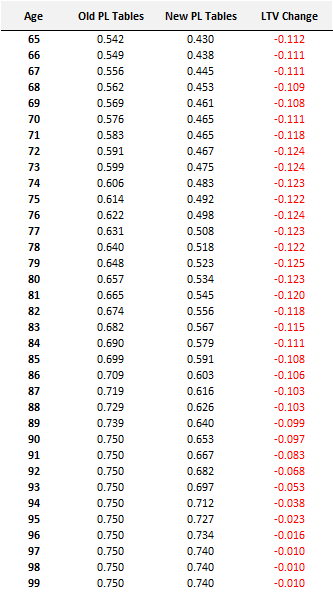

Principal Limit Tables Have Been Revised

The principal limit is the total amount of proceeds initially available to a reverse mortgage borrower. The principal limit is determined by multiplying the maximum claim amount by a principal limit factor, or PL factor, which is set by FHA.

As an example, let’s assume the maximum claim amount is $300,000 and the PL factor is 0.50 based on the youngest borrower’s age and the expected interest rate (EIR). The PL factor is multiplied by the maximum claim amount to arrive at an initial proceeds amount of $150,000 (0.50 * $300,000), which is the principal limit. These proceeds would then be divvied up to cover existing mortgage balances, closing costs, required property charges, and any allocations to the borrower in the form of cash or line of credit.

As of October 2, 2017, FHA has completely revised the principal limit factor tables. Most borrowers will see at least some reduction in principal limit under the new tables, which means there may be less money available under the reverse mortgage program now than in the past. The table shows a comparison of old PL factors versus the new PL factors. Note that this comparison assumes an EIR of 5%, which is appropriate for today’s market.

As of October 2, 2017, FHA has completely revised the principal limit factor tables. Most borrowers will see at least some reduction in principal limit under the new tables, which means there may be less money available under the reverse mortgage program now than in the past. The table shows a comparison of old PL factors versus the new PL factors. Note that this comparison assumes an EIR of 5%, which is appropriate for today’s market.

To understand the impact of this, think of the PL factor like loan-to-value. In other words, it’s a percentage of the maximum claim amount. For example, if the PL factor is 0.500, then the principal limit is 50% of the maximum claim amount. For a $200,000 house, the principal limit would be $100,000. For a 65-year old borrower, the PL factor has been reduced by 0.112. Assuming a $200,000 home value, that means a reduction in proceeds of $22,400 versus a week ago.

Is a HECM Still a Good Deal?

With all the changes, including the substantial reduction in principal limits, is the HECM a good deal anymore? Well, that depends! It depends on your goals and financial situation. Yes, you’ll likely qualify for less now than in the past, but if a HECM still accomplishes your financial goals and puts you in a better financial position, then it absolutely can be a fantastic financial tool.

If anything, I think the recent changes really argue for the urgency of taking advantage of a HECM now if it makes sense. Don’t assume today’s reverse mortgage will be here tomorrow – because it likely won’t! FHA is constantly fine-tuning the program, and the result has been less money and more qualification requirements over the years.

If a HECM makes sense for you today, then absolutely take advantage of it.