Loan level price adjustments, or LLPAs, are largely invisible to mortgage borrowers, but they can add thousands to the cost of a mortgage. We’ll cover what loan level price adjustments are and how they work so you can position yourself to get the best mortgage deal possible.

Table of Contents

What is a Loan Level Price Adjustment (LLPA)?

LLPAs are charges for certain risk factors such as low credit scores, loan-to-value, combined loan-to-value, investment property, etc. LLPAs are typically assessed as a percentage of the loan amount.

You may also hear mortgage professionals refer to LLPAs as risk-based pricing.

If you hear the term “LLPA” or “loan-level price adjustment”, it’s most likely in the context of Fannie Mae or Freddie Mac conventional mortgage financing. However, government-backed FHA and VA mortgages also have their own similar form of risk-based pricing.

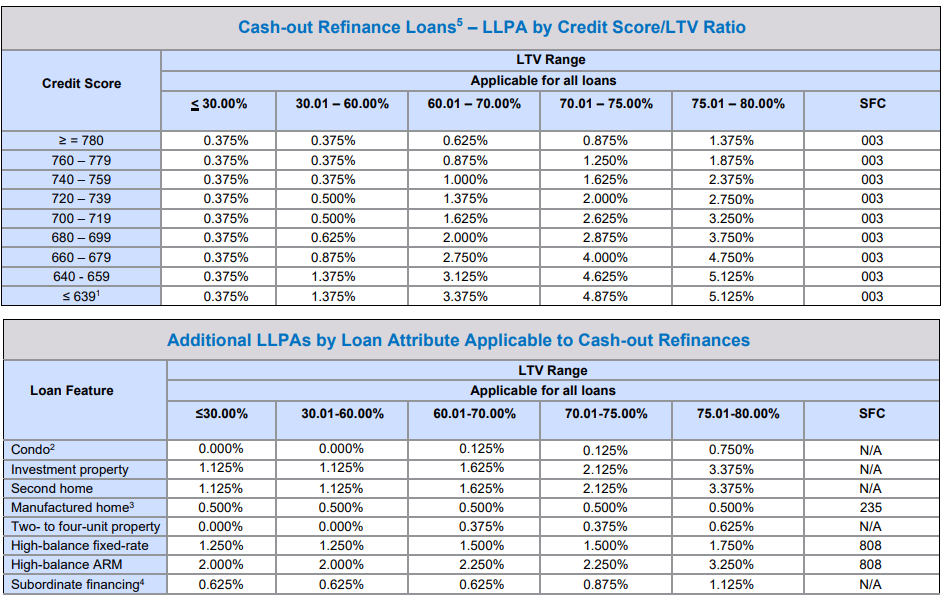

To see how loan level price adjustments work, let’s check out an example. Let’s assume we have two homeowners who are both borrowing $100,000 using cash out refinances with loan-to-values of 75%.

Their qualifications are exactly the same in every respect except for their credit scores: one has a credit score of 780 and the other has a credit score of 639.

The chart below is from the latest (as of this writing) Fannie Mae LLPA matrix. On the left side of the chart, you’ll see a list of credit score ranges. Across the top of the chart, you’ll see a range of loan-to-values.

You’ll notice that for a credit score of 780, there’s a loan level price adjustment of 0.875% for a loan-to-value of 75.00%. To calculate the cost of the price adjustment, we simply multiply it by the loan amount:

0.875% (LLPA) * $100,000 (loan amount) = $875 (LLPA cost)

As you can see, the cost of the price adjustment for this scenario is $875.

Now let’s check out what the pricing looks like for the 639 credit score. Referring to the matrix again, you’ll see that the price adjustment for a 639 credit score and a 75.00% loan-to-value is a whopping 4.875%.

Again, to calculate the cost of the LLPA, we simply multiply it by the loan amount:

4.875% (LLPA) * $100,000 (loan amount) = $4,875 (LLPA cost)

It’s pretty obvious Fannie Mae considers a 639 credit score to be much riskier than a 780 credit score.

LLPA charges are calculated in the form of “points”, but it doesn’t mean they’re ultimately paid that way. Lenders often cover the cost of some or all applicable LLPAs by using yield spread. To see how this works, let’s check out another example.

| Interest Rate | Yield Spread |

| 4.750% | 0.750% |

| 4.875% | 0.250% |

| 5.000% | 0.000% |

| 5.125% | (0.250%) |

| 5.250% | (0.625%) |

The table shows a hypothetical lender rate sheet with interest rates ranging from 4.750% to 5.250%. The left side of the table shows the various interest rates available and the right side of the table shows the corresponding yield spread for each interest rate.

As you can see, the lowest rate is 4.750% and it has a positive yield spread of 0.750%. That means the 4.750% interest rate comes with a cost of 0.750%.

The highest rate on the rate sheet, 5.250%, has a negative yield spread of 0.625%. A negative yield spread is a credit. It’s essentially a rebate from the lender used to cover risk-based pricing and other closing costs.

Like LLPAs, yield spread is calculated as a percentage of the loan amount. For example, the 0.750% cost for the 4.750% interest rate equals 0.750% of the loan amount. If the loan amount is $100,000, the cost for the 4.750% rate is $750.

On the other hand, the 5.250% interest rate has a rebate of 0.625%, which equals 0.625% of the loan amount. Again, if the loan amount is $100,000, then you get $625 from the lender to cover risk-based pricing and other closing costs.

Lenders commonly use yield spread to cover loan level price adjustments and reduce the upfront costs of the loan. To see how this works, let’s calculate the net costs, including yield spread and LLPA, for our borrower with the 780 credit score. Again, we’re assuming the following for this borrower:

- Credit score: 780

- Loan-to-value: 75%

- Loan amount: $100,000

Here’s how the net pricing works out, taking into account LLPAs and yield spread:

| Interest Rate | Yield Spread | LLPA Total | % Cost/Points | $ Cost |

| 4.750% | 0.750% | 0.875% | 1.625% | $1,625 |

| 4.875% | 0.250% | 0.875% | 1.125% | $1,125 |

| 5.000% | 0.000% | 0.875% | 0.875% | $875 |

| 5.125% | (0.250%) | 0.875% | 0.625% | $625 |

| 5.250% | (0.625%) | 0.875% | 0.250% | $250 |

If this borrower chooses the 4.875% rate, the net cost of the risk-based pricing and yield spread will be 1.125 points, or $1,125 on a loan amount of $100,000. This cost is in addition to any other closing costs.

Now, let’s see how this looks for our borrower with the 639 credit score. Again, here’s the assumptions we’re working with:

- Credit score: 639

- Loan-to-value: 75%

- Loan amount: $100,000

Here’s how the net pricing works out, taking into account LLPA and yield spread:

| Interest Rate | Yield Spread | LLPA Total | % Cost/Points | $ Cost |

| 4.750% | 0.750% | 4.875% | 5.625% | $5,625 |

| 4.875% | 0.250% | 4.875% | 5.125% | $5,125 |

| 5.000% | 0.000% | 4.875% | 4.875% | $4,875 |

| 5.125% | (0.250%) | 4.875% | 4.625% | $4,625 |

| 5.250% | (0.625%) | 4.875% | 4.250% | $4,250 |

As you can see, the costs are pretty steep no matter which interest rate this borrower chooses. If this borrower wants to keep his closing costs relatively low, then he probably wants to go with the 5.250% interest rate. That’s the highest rate on the rate sheet, but the closing costs are about $1,400 cheaper.

Yield spread is the reason lenders can offer so-called “no cost” loans. Such loans aren’t truly “no cost” because you’re essentially paying a slightly higher interest rate so the lender will cover your closing costs.

Today’s Interest Rates

Want to see more options? Check all mortgage rates here

3 Ways LLPAs Can Cost You

As we’ve covered, LLPAs are essentially charges for various risk factors, including credit scores, loan-to-value, property type, etc. Lenders don’t typically break down the applicable risk-based pricing when you apply for a loan, so it’s not always obvious how it impacts your loan costs. Here are the three ways LLPAs can potentially cost you thousands (or tens of thousands) over the life of a home loan:

- Closing costs: LLPAs are charged as a percentage of the loan amount. They often show up in the form of “points” on your Loan Estimate and can potentially add thousands to your closing costs, especially if you have low credit scores.

- Interest rate: Lenders don’t offer just one interest rate. They offer a series of interest rates with various yield spreads. The lowest rates usually have a positive yield spread, which means there’s an additional cost to get that interest rate. The highest rates usually offer a negative yield spread, which means you get a credit to offset risk-based pricing and other closing costs. If the risk-based pricing is steep, lenders commonly offer a higher interest rate to either reduce the yield spread cost or get a credit that can be used to offset the LLPAs. This is how LLPAs can impact the interest rate you pay for a mortgage.

- Interest rate and closing costs: Risk-based pricing can impact the closing costs, the interest rate, or some combination of both. If the total LLPAs are expensive, the lender may not have a rate available with enough yield spread to cover all of the risk-based pricing. In such cases, the pricing adjustments will increase both the interest rate and the closing costs.

For more information about how LLPAs work, check out the video below.

The “Perfect” Loan Scenario

Is there such thing as a “perfect” loan scenario where risk-based pricing doesn’t apply? Absolutely! If you’re purchasing a single-family home, there are no pricing “hits” at all if you put down at least 25% and have a credit score of 780 or better.

If you’re refinancing a single-family home and not taking out cash, there are no price adjustments if your loan-to-value is 70% or less and your credit scores are 780 and better.

This is why it’s super important to keep your credit scores as strong as possible. Credit scores are one of the biggest factors that determine how much you’ll pay for closing costs and interest rate. The difference between a 720 and a 780 credit score can be thousands or even tens of thousands of dollars over the life of the loan.

Frequently Asked Questions

What does LLPA mean in mortgage?

A loan level price adjustment, or LLPA, is essentially a charge for certain mortgage qualifying risk factors, such as low credit scores, high loan-to-value, property type, etc. LLPAs are charged as a percentage of the loan amount and are paid in the form of closing costs, a higher rate, or some combination of the two.

Does LLPA affect interest rate?

A loan level price adjustment, or LLPA, is essentially a charge for certain mortgage qualifying risk factors, such as low credit scores, high loan-to-value, property type, etc. LLPAs are charged as a percentage of the loan amount and are paid in the form of closing costs, a higher rate, or some combination of the two. Yes, LLPAs can impact the interest rate you’re charged for a mortgage.

Will LLPA affect my current mortgage?

Fannie Mae occasionally changes their loan level price adjustments, or LLPAs, but the changes have no impact on existing conventional mortgages. The changes only impact new conventional mortgages.