What if I said there was a way to turn a large portion of your home’s equity into a liquid and tax free retirement account that grows larger over time? Would you believe me? If not, I wouldn’t hold it against you!

I want to show you a retirement strategy that many people, including financial advisers, are completely unaware of. Thousands of homeowners across the country are using this strategy right now to create a more financially-secure retirement.

The unusable asset

Think about your home’s equity for a minute. How does it make your life better? Whether your home equity equals $500 or $500,000, what real impact does it have on your day-to-day lifestyle? Probably not much, right?

Your home equity is largely just a number on paper if you’re not planning to sell your home. It may be a very nice number, but it has no real impact on your day-to-day life. Unless you can convert your home equity into cash, you can’t use it to buy groceries or book a plane ticket to Hawaii.

Having said that, there’s certainly nothing wrong with having a lot of equity in your home. It’s very commendable to pay off your home and no longer have a mortgage payment. In a sense, home equity serves as a forced savings account that you contribute to with every mortgage payment you make.

The problem with home equity is that it’s an unusable savings account. It can’t normally be converted to cash without either selling the home or doing a “cash out” refinance. Obviously, selling makes no sense if you want to continue living in your home. A “cash out” refinance can sometimes make sense, but it comes with the downside of a mortgage payment for 30 years.

However, there is a way to access home equity without having to sell or take on a mortgage payment. Even better, you can convert a large portion of your equity into a tax free retirement account that will grow larger over time.

How? With a reverse mortgage.

Now, bear with me. If you’re like many people, you’ve probably heard few positives about a reverse mortgage. I’ll grant that some of what you’ve heard could be justified, but I guarantee most of it is not. There is a ton of misinformation out there about reverse mortgages. My hope is that you’ll have an open mind and let me show you how a reverse mortgage can fit into your financial plan.

What it is and how it works

The most common reverse mortgage product in America today is the home equity conversion mortgage, or HECM (often pronounced heck-um by industry insiders). If somebody you know recently got a reverse mortgage, it’s likely it was a HECM.

The HECM program was signed into law by President Reagan as part of the Housing and Community Development Act of 1987. Today, the program is overseen and regulated by the Federal Housing Administration (FHA) under the authority of the Department of Housing and Urban Development (HUD). Over 50,000 HECM reverse mortgages are written every year in America today.

If you’re at least 62, the HECM enables you to convert a portion of your home’s value into tax free cash without selling or taking on a mortgage payment. No mortgage payments are required as long as you live in the home and pay the required property charges.

You always remain the owner of your home, which means you’re free to leave it to your heirs. Your heirs will inherit any equity remaining in the home.

The HECM is a non-recourse loan. FHA covers the shortage if your home isn’t worth enough to cover the loan balance.

HECM proceeds have no impact on income taxes, Medicare, or Social Security retirement benefits.

Proceeds can be taken as a line of credit, lump sum, monthly term/tenure income, or a combination of these options. We’ll focus on the line of credit next.

The home equity tax free retirement account

The HECM line of credit is similar to a traditional home equity line of credit (HELOC), but without the pitfalls and risks. Now, here’s the best part: the unused HECM credit line will automatically grow and compound larger with no limit based on an annual growth rate.

Note that the lender isn’t taking money from your equity and investing it for you. They’re simply increasing your available credit line automatically based on an annual percentage rate.

The growth has nothing to do with home values; your home’s value could fall and your available credit will still grow as long as you meet your program obligations.

The growth has nothing to do with home values; your home’s value could fall and your available credit will still grow as long as you meet your program obligations.

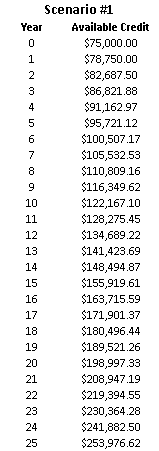

To see how the growth works, let’s check out an example. Let’s assume you qualify for an initial credit line amount of $75,000 and an annual growth rate of 5%. As you can see in Figure 1, the line of credit will grow to over $95,000 after just five years. After ten years, it will be worth over $122,000!

Because the growth rate applies to your available line of credit, growth compounds on growth. This means the available credit can really pile up over time.

The growth rate will also keep up with prevailing interest rates. If interest rates rise in the future, the growth rate will as well. This means your line of credit will grow even faster!

Because there’s no limit on growth, it’s possible the line of credit could grow larger than the value of your home. And because the HECM is non-recourse, you, your estate, and your heirs are not on the hook for the shortage if your home isn’t worth enough to settle the entire loan balance.

For another example, let’s assume your line of credit starts off at $150,000 and the growth rate is again 5%. As you can see in Figure 2, the growth really adds up quickly. After just five years, your available credit line will be worth over $191,000. After ten years, it’s worth more than a whopping $244,000!

For another example, let’s assume your line of credit starts off at $150,000 and the growth rate is again 5%. As you can see in Figure 2, the growth really adds up quickly. After just five years, your available credit line will be worth over $191,000. After ten years, it’s worth more than a whopping $244,000!

At the end of 20 years, you would have just shy of $400,000 available tax free with just a phone call. Wow!

More liquid assets equals more financially security

The HECM line of credit is a fantastic financial tool that can substantially add to your liquid retirement assets. As we’ve seen, it essentially turns home equity into a liquid and tax free retirement account that grows automatically. More liquid assets equals more financial security at a time in life when home maintenance, medical expenses, and long-term care can be a huge financial burden.

If you’re at least 62 and owe little to nothing on your home, a HECM line of credit could benefit you enormously – especially if you don’t need the money right now. Get the line of credit set up and let it grow and compound. By the time you need the money, you’ll have substantially more than you started with.