The reverse mortgage residual income (RI) requirements are a key component of the FHA reverse mortgage lending requirements. So what are the requirements? How does residual income work? Why is it important?

Residual income was implemented with the new financial assessment guidelines rolled out in 2014. It’s important because it helps lenders determine if you have the financial ability to pay your property charges.

If your residual income doesn’t meet FHA’s requirements, your lender may require a life expectancy set-aside (LESA). A LESA can be avoided if you can document certain compensating factors that make up for the residual income shortfall. If one or more compensating factors cannot be documented, a LESA may be required or you may not qualify at all (depending on the seriousness of the income shortfall).

The qualifying requirements

Residual income is calculated by adding up your monthly income and deducting debt payments (excluding mortgage payments to be eliminated by the reverse mortgage), monthly property charges, and an estimate of utility and maintenance costs. Utility and maintenance costs are estimated based on the region and square footage of the home.

Residual income is calculated by adding up your monthly income and deducting debt payments (excluding mortgage payments to be eliminated by the reverse mortgage), monthly property charges, and an estimate of utility and maintenance costs. Utility and maintenance costs are estimated based on the region and square footage of the home.

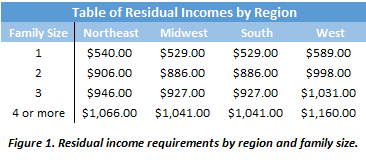

The remaining residual income must meet a certain threshold based on the region where you live and the number of people living in your home. Figure 1 shows the required thresholds by region and household size.

Calculating residual income

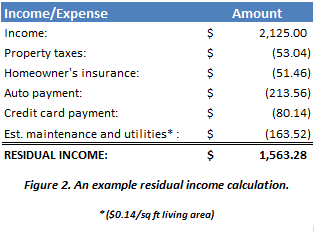

Let’s look at an example of a residual income calculation. Let’s assume we’re working with a couple who lives in a 1,168 square foot home and has $2,125/month in total Social Security income. Let’s also assume this couple lives in Texas, which is in FHA’s South region.

Figure 2 shows a breakdown of their monthly expenses. After the property charges, debt payments, and estimated maintenance and utilities are backed out, they are left with $1563.28 in disposable income.

Based on Figure 1, a household size of 2 in the South region needs to have at least $886/month in disposable income to qualify. As you can see, this couple clearly meets the reverse mortgage residual income requirements.

Student loans

If you have student loans, your lender will need to account for the payments when calculating your residual income. If your payments are deferred, your lender will use a calculated payment for qualifying purposes. Lenders require this because they want to ensure you have the financial ability to pay your property charge payments even after your student loan payments begin again. Here’s how your student loan payments will likely be handled:

- If a payment greater than zero is reported on your credit report, the lender will use that payment for the residual income calculation. If your actual payment is less (but still greater than zero), your lender can use the smaller payment as long as you provide documentation from your servicer proving the smaller payment.

- If the monthly payment is zero, the lender will assume a payment of 0.5% of the outstanding balance for the residual income calculation. For example, if the student loan balance is $10,000, the assumed payment will be $50 for qualifying purposes.

As you can see, the lender may assume a payment for the residual income calculation even if you’re not required to actually make payments on your student loans. This requirement can sometimes make it difficult to qualify if you have a large amount of student loan debt.

Collections

Collection accounts are delinquent unpaid debts that have been purchased from the original creditor by a collection agency. Collection agencies usually don’t report payments for collection debts, so your lender will likely assume a payment for the residual income calculation. If the total aggregate collection balances are $2,000 or more, the lender will use a payment equal to 5% of the collection balances for the residual income calculation. If you have a lot of collection debt, this can potentially make it difficult to meet the residual income qualification requirements.

Charge offs and repossessions

Charge offs and repossessions are unpaid derogatory debts that usually do not have payments reported on a credit report. These types of debts are usually written off by the original creditor, so the lender will not assume a any kind of payment for the residual income calculation.

What if income comes up short?

What happens if your residual income comes up short because of high debt or low income? It’s still possible to qualify, but you may need to document one or more compensating factors. Such factors can include income from other sources, unused proceeds available in the reverse mortgage after closing, available cash in retirement accounts or savings, etc. If your residual income is still short after applying compensating factors, your lender may require a LESA or you may not qualify at all.