The reverse mortgage industry is a relatively small niche of the broader mortgage industry. Though many mortgage lenders offer HECM reverse mortgages (the dominant product in the industry), relatively few have been able to build large and consistent businesses around the product. About 50% of all reverse mortgages written in 2016 were by the top 5 lenders.

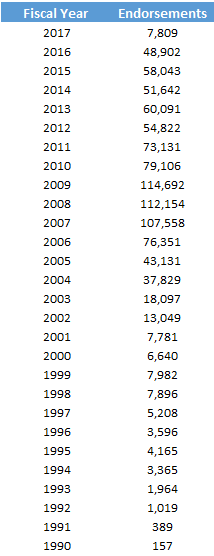

So, how many reverse mortgages are done each year in the United States? Volume has dropped significantly since the peak of the housing boom and the financial crisis in 2008, but the industry as a whole is currently averaging around 50,000 to 60,000 HECMs per year.

Having said that, there is enormous growth potential in the future. The American population continues to grow older and many homeowner’s at or near retirement age don’t have enough money saved to last their entire retirement.

Humble Beginnings

The HECM reverse mortgage came into being with the passage of the Housing and Community Development Act of 1987, which authorized the Department of Housing and Urban Development (HUD) to start an FHA-insured reverse mortgage pilot program. At first, the program was only available through a few select lenders and FHA was authorized to endorse up to just 2500 HECMs.

As time passed and the program proved viable, Congress gradually increased the endorsement volume cap. By 1998, the HECM program had been made permanent and the volume cap raised to 150,000 HECMs.

The volume cap was raised yet again to 275,000 HECMs in 2006.

Endorsements peaked at just a little over 114,000 HECMs in fiscal year 2009 (see the table at right). Volume dropped considerably after 2009 as the financial crisis and housing bust took hold.

More recent changes in regulations and lending guidelines have impacted industry volume as well.

Enormous Growth Potential

Though reverse mortgage endorsements have declined since 2009, they’ve stabilized at around 50,000 to 60,000 HECMs every fiscal year.

An MIT study concluded that reverse mortgages have only achieved around a 2% potential market penetration thus far. With the US population aging and many retirees (or soon to be retirees) not saving enough, the reverse mortgage could play a key retirement planning role in the future.

As long as interest rates stay reasonably low, there could be enormous growth potential in the reverse mortgage space in the coming years and decades.

Note: The endorsement numbers in the table are based on the federal government’s fiscal year, which runs from October 1 to September 30.

Source: NRMLA